The Truth About CMG Mortgage for First-Time & Repeat Buyers

Picking a home lender can feel like picking a doctor you have never met. You hand over your income, your credit history, and your biggest financial decision, and you hope they treat you right. Maybe you saw the name CMG Mortgage while comparing lenders and wondered if it is the real deal or just another name on a long list. A close friend of mine asked me this same question last spring before she bought her first house, and I watched her dig through forums for two weeks looking for a straight answer. This guide gives you that straight answer in one place.

By the end, you will know how its rates, loan programs, fees, and customer service stack up in 2026. You will also see its two signature products that almost no other lender offers, along with real pros and cons. No fluff, no sales pitch, just the facts you need to decide if this lender fits your home loan plans.

CMG Mortgage at a Glance

CMG Mortgage, often shown to customers under the brand name CMG Home Loans, is a national mortgage lender based in California. The company has funded home loans since 1993, which gives it over three decades in the business. It operates in most states and works through a network of local loan officers rather than a faceless call center. This local-officer model is one reason many borrowers say their experience felt personal instead of rushed.

The lender holds licenses to handle conventional, government-backed, and jumbo loans. It also built two products you will not find at most banks, which we cover further down this guide. Loan officers here tend to specialize by region, so the person helping you usually understands local home prices and local closing rules.

CMG Mortgage Rates 2026

Mortgage rates change daily, and no lender can promise an exact number without pulling your credit and details. That said, CMG Mortgage rates in 2026 generally track close to the national average for similar credit profiles. Borrowers with strong credit scores and steady income tend to see the most competitive offers, while lower credit scores usually mean a higher rate.

Here is a simple look at how rate ranges tend to break down by loan type this year. Treat these as a starting point, not a locked offer, since your real rate depends on credit score, down payment, and loan amount.

| Loan Type | Typical Rate Range (2026) | Best For |

|---|---|---|

| Conventional 30-Year | Mid-range, near national average | Buyers with good credit and steady income |

| FHA Loan | Slightly below conventional | First-time buyers with lower credit scores |

| VA Loan | Often the lowest of all types | Eligible veterans and service members |

| Jumbo Loan | Slightly above conventional | High-value home purchases |

The smartest move is to request a rate quote directly and compare it against two or three other lenders on the same day. Rate shopping within a short window will not hurt your credit score much, since credit bureaus group mortgage inquiries together.

CMG Loan Programs: Full Breakdown

CMG offers nearly every common loan type, plus a few programs that go beyond the basics. Below is a plain breakdown of each option so you can spot which one fits your situation.

Conventional Loans

Conventional loans are not backed by the government and usually need a credit score around 620 or higher. Down payments can start as low as 3% for qualified first-time buyers. These loans work well for buyers with steady jobs and decent credit history.

FHA Loans

FHA loans are backed by the Federal Housing Administration and accept credit scores as low as 580 in many cases. Down payments can be as low as 3.5%. This program suits buyers who are still building their credit or savings.

VA Loans

VA loans serve eligible veterans, active service members, and some surviving spouses. Most VA loans need zero down payment, which is a major advantage. There is also no monthly mortgage insurance, which keeps the payment lower over time.

USDA Loans

USDA loans target buyers in eligible rural and suburban areas. Like VA loans, they often require no down payment at all. Income limits apply, so check your local area before assuming you qualify.

Jumbo Loans

Jumbo loans cover home prices above the standard conforming loan limit. These loans usually need stronger credit and a larger down payment. Buyers in expensive housing markets often need this option.

Non-QM & Medical Professional Mortgage

Non-QM loans help self-employed buyers, gig workers, and investors who cannot show traditional pay stubs. CMG also runs a special mortgage track for doctors, dentists, and other medical professionals, often with reduced down payment rules. This program recognizes that high-earning professionals sometimes carry student debt that standard underwriting rules would otherwise penalize.

CMG’s Signature Products: What No Other Lender Offers

This is where CMG truly stands apart from typical banks and online lenders. The company built two products that you simply cannot get elsewhere under the same terms.

The All In One Loan — CMG’s Patented Mortgage

The All In One Loan combines your mortgage with a checking account, working like a giant line of credit against your home equity. Every dollar you deposit reduces your loan balance immediately, which cuts the interest you pay each day. Many financially disciplined borrowers use this to pay off their home years faster than a standard 30-year loan. It is a patented structure, so you will not find an identical version at another lender.

HomeFundIt — Crowdfunding Your Down Payment

HomeFundIt lets you create a personal fundraising page so friends and family can gift money toward your down payment. Contributions are tracked and documented properly, which solves the usual paperwork headache around gift funds. This tool is especially useful for first-time buyers who do not have large savings but have a generous support network. It turns a wedding-registry style idea into real down payment assistance programs.

CMG Rate Rebound (No-Lender-Cost Refinance)

Rate Rebound allows certain borrowers to refinance later at no extra lender cost if rates drop after closing. This removes the fear of locking in today only to feel stuck if rates fall next year. Eligibility rules apply, so ask your loan officer for the exact terms tied to your loan.

Down Payment Assistance & First-Time Buyer Options

First-time buyers often assume they need 20% down, but that is rarely true anymore. Between FHA loans, conventional 3% down options, and tools like HomeFundIt, many buyers close with far less saved up. Some state and local programs can pair with a CMG loan to cover part of the down payment or closing costs.

A loan officer can check which local programs apply in your area, since rules vary widely by state. It is worth asking about this even if you think you will not qualify, because many programs have higher income limits than people expect.

CMG HELOC & Refinance Options

Beyond purchase loans, the lender offers ways to tap your existing home equity or lower your current payment.

5-Day HELOC

The 5-Day HELOC promises a fast closing timeline for a home equity line of credit, often within five business days from approval. This speed matters if you need cash quickly for a renovation, debt payoff, or emergency expense. Traditional HELOCs from banks can take weeks, so this turnaround stands out.

Cash-Out Refinance vs. HELOC — Which Makes Sense

A cash-out refinance replaces your entire mortgage with a new, larger one and gives you the difference in cash. A home equity line of credit, on the other hand, sits as a second loan on top of your existing mortgage. Cash-out refinancing often makes sense when current rates are lower than your existing rate. A HELOC tends to make more sense when your existing rate is already low and you do not want to disturb it.

CMG Mortgage Requirements: Do You Qualify?

Qualifying depends heavily on which loan program you choose, but here are general guidelines borrowers can expect from CMG Mortgage in 2026.

- Credit score of 580 or higher for FHA loans, 620 or higher for most conventional loans

- Debt-to-income ratio generally under 45%, though exceptions exist for strong applicants

- Steady income history, usually two years of documentation for employed and self-employed borrowers

- Down payment ranging from 0% for VA and USDA loans up to standard amounts for jumbo loans

- Sufficient cash reserves for certain non-QM and jumbo programs

These are general benchmarks, not guarantees. The only way to know your exact standing is to get pre-approved and let an underwriter review your full file.

CMG Mortgage Fees: The True Cost of Borrowing

Every mortgage comes with closing costs, and CMG Mortgage is no exception. Typical fees include an origination charge, underwriting fee, appraisal cost, title insurance, and prepaid items like property taxes and homeowners insurance. These usually add up to roughly 2% to 5% of your total loan amount, which lines up with the broader mortgage industry.

- Origination fee: covers processing your application

- Underwriting fee: covers reviewing and approving your loan file

- Appraisal fee: pays for an independent home value check

- Title and escrow fees: protect ownership and hold funds during closing

- Prepaid taxes and insurance: collected upfront to start your escrow account

Ask for a Loan Estimate early in the process so you can compare these fees against other lenders side by side. A slightly higher rate with lower fees can sometimes beat a lower rate loaded with extra charges.

How to Apply for a CMG Mortgage

- Reach out to a local CMG loan officer through the company website or a referral.

- Gather your income documents, bank statements, and identification before your first call.

- Get pre-approved so you know your real budget before house hunting.

- Choose your loan program based on your credit, down payment, and goals.

- Submit your full application and respond quickly to any underwriter requests.

- Lock your rate once you are comfortable with the terms.

- Close on your loan and move into your new home.

If you get stuck anywhere in this process or want a second opinion before signing anything, you can also reach our editorial team at james@allthings-mortgage.com for general guidance.

CMG Mortgage Customer Reviews & Complaints

Customer feedback on CMG Mortgage tends to be mixed, which is normal for any large national lender. Many reviewers praise their individual loan officer for clear communication and a smooth closing. Common complaints involve slow communication during underwriting and occasional confusion when a loan transfers to a new servicer after closing.

Before choosing any lender, it helps to read recent reviews on independent sites rather than relying only on the lender’s own testimonials. Pay closer attention to how the company responds to complaints than to the complaints themselves, since every large lender collects some negative reviews over time.

CMG Mortgage Servicing: Life After Closing

Like most large lenders, your loan may get transferred to a different servicer after closing, which is standard across the mortgage industry and not unique to this company. You will receive written notice before any transfer, and your loan terms cannot legally change because of it. If you ever feel confused after a servicing transfer, our guide on PHH Mortgage Services explains exactly what borrowers should expect when a new company takes over their payments.

Keep your closing documents safe and note your loan number, since you will need it for any future servicing questions. Setting up automatic payments early can also prevent missed payments during a confusing transfer period.

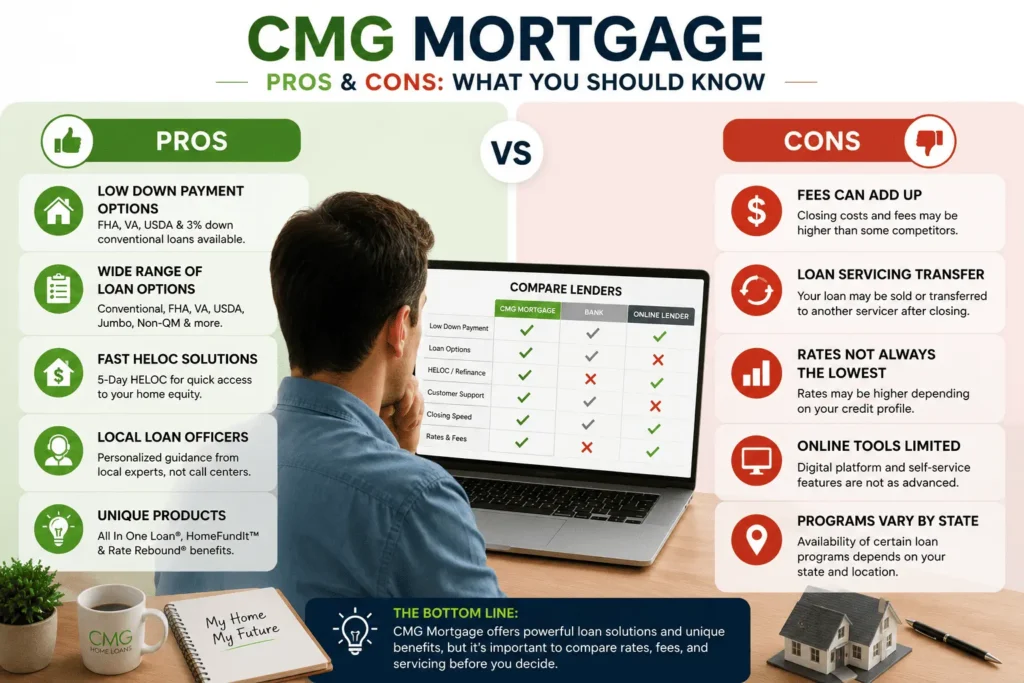

CMG Mortgage Pros & Cons

Pros

- Unique products like the All In One Loan and HomeFundIt that few competitors match

- Wide range of loan programs, including VA, USDA, and non-QM options

- Local loan officers who often provide personal, hands-on service

- Fast 5-Day HELOC turnaround for existing homeowners

Cons

- Rates are not always the lowest on the market for every credit profile

- Loans may transfer to a different servicer after closing

- Online self-service tools are less developed compared to big tech-first lenders

- Availability of certain programs depends on your state

CMG Mortgage vs. Top Competitors

Comparing lenders side by side makes the decision much clearer than reading reviews alone.

| Feature | CMG Mortgage | Typical Big Bank | Online-Only Lender |

|---|---|---|---|

| Loan Officer Access | Local, personal | Branch-based | Mostly remote |

| Unique Products | All In One Loan, HomeFundIt | Rare | Rare |

| Government Loans | Yes, full range | Limited at some banks | Varies |

| Closing Speed | Average to fast | Average | Often fast |

| Down Payment Help | HomeFundIt crowdfunding | Rare | Rare |

If you want a lender with creative tools and a personal touch, this company holds an edge. If you mainly want the absolute lowest possible rate and do not mind a digital-only process, it is still worth comparing offers from a Flat Branch Mortgage rates guide alongside this one before deciding.

Conclusion

We started this guide by asking whether CMG Mortgage deserves your trust, and now you have the full picture to answer that yourself. You have seen its rates, loan programs, fees, signature products, and honest pros and cons side by side. This lender stands out most for buyers who want creative tools like the All In One Loan or need flexible down payment help through home equity line of credit options and crowdfunding. Compare a real quote against two other lenders, and you will know within a week if this is the right fit for your home loan.

Frequently Asked Questions

Is CMG Mortgage a legitimate company?

Yes. It has operated since 1993 and is a licensed national lender offering conventional, government-backed, and specialty loans. It is regulated like any other mortgage company and reports to standard industry oversight bodies across the country.

What credit score does CMG require?

Minimum scores depend on the loan type. FHA loans can accept scores as low as 580, while conventional loans typically need 620 or higher. Jumbo and non-QM loans often require stronger credit profiles to qualify for approval.

Does CMG sell its loans after closing?

Like most lenders, loans may be sold or transferred to a different servicer after closing. This is standard industry practice and does not change your interest rate, loan terms, or remaining balance in any way.

How long does CMG take to close a loan?

Closing timelines usually range between three and six weeks, depending on the loan type and how quickly documents are submitted. The 5-Day HELOC product moves much faster since it serves a different, smaller approval process.

What makes CMG different from other lenders?

Its patented All In One Loan and HomeFundIt crowdfunding tool set it apart from typical banks. Few competitors offer either product, making this lender a strong pick for buyers wanting creative financing solutions beyond a standard mortgage.