Master Your 21st Mortgage Payment Without Stress or Confusion

My cousin bought a manufactured home last year and got her loan through 21st Mortgage. A few months in, she called me confused. She didn’t know if she could pay online, why her bill went up one month, or what number to call when a payment failed to go through. She wasn’t sure how her 21st mortgage payment actually worked, and honestly, neither was I until I looked into it myself.

This guide walks you through every part of it. You’ll learn how to pay, what happens if you’re late, how escrow changes your bill, and who to call when something goes wrong. By the end, you’ll know exactly how to manage your loan without guessing, and you won’t have to call around for basic answers like she did.

I’ve spent years covering mortgage servicing topics for manufactured and mobile home buyers, and 21st Mortgage comes up more than most lenders because of how specific its process is. Every number, address, and step listed here comes directly from the company’s own official pages and forms. Nothing here is a guess, and I’ve double-checked each detail against the source before writing it down.

Who Is 21st Mortgage?

21st Mortgage Corporation started in Knoxville, Tennessee, back in 1995. Today it’s one of the largest lenders for manufactured and mobile home loans in the country. The company is owned by Berkshire Hathaway, which gives it strong financial backing behind every loan it services.

You might also see it written online as “21st century mortgage,” but that’s just a common mix-up people type by mistake. The real name is 21st Mortgage Corporation, and its NMLS number is 2280. It offers FHA, VA, USDA, and conventional loans for manufactured homes, plus refinancing and equity options.

21st Mortgage Corporation payments are handled entirely through their own servicing system, not a separate billing company. Knowing this matters because it explains why the payment tools work the way they do. Manufactured home loans often follow different rules than regular mortgages, and the payment system was built around that.

The company started small, with just four employees in downtown Knoxville back in 1995. It has since grown into a team of over 800 people spread across two campuses. That growth matters because it means more staff available to answer calls and process payments without long delays.

If you’re still comparing 21st Mortgage against other lenders, our full 21st Mortgage review breaks down rates, credit requirements, and loan types in more detail.

Ways to Pay Your 21st Mortgage Bill

There are several ways to handle a 21st mortgage payment, and you don’t have to stick to just one. Some borrowers like paying online because it’s fast. Others prefer calling in or mailing a check the old-fashioned way. Their online bill pay portal, along with phone and mail, covers most situations.

- Pay online through the Account Access portal

- Pay by phone, live agent or automated system

- Mail a check to their payment processing address

- Set up autodraft for automatic withdrawals

Making a Payment Online Through Account Access

The easiest way to pay online is through the Account Access portal on 21stmortgage.com. You’ll need your loan number and a few personal details to set up your login the first time. For 21st Mortgage Corporation online payments, this portal is the fastest option available.

Once you’re in, you can see your balance, due date, and payment history in one place. The portal also lets you make a one-time payment straight from your checking or savings account. This works well if you want a quick pay option without picking up the phone.

Keep in mind the portal doesn’t currently support debit or credit cards. You’ll need to link a bank account instead. Most borrowers find this setup simple once it’s done the first time.

Paying by Phone — Live Agent vs Automated System

If you’d rather talk to someone, call 1-800-955-0021 between 8 a.m. and 8 p.m. Eastern time. A financial counselor can walk you through your balance and help you make a payment right then.

There’s also an automated phone system if you just want to pay without waiting on hold. That number is 1-866-380-0373, and it runs longer hours than the live line. Both options pull payment directly from your bank account.

Phone payments are a solid backup when the website is down or you’re away from a computer. Just have your loan number ready before you call.

Sending a Payment by Mail

Some borrowers still prefer mailing a check, especially if they’ve done it for years. Regular payments go to 21st Mortgage Payment Processing, 620 Market Street, Knoxville, TN 37902.

Mail can take a few extra days to process, so send it early if your due date is close. Always write your loan number on the check so it gets applied to the right account. This method works fine, but it’s the slowest of the three.

Is Credit or Debit Card Payment Accepted?

This is one of the most searched questions, and the short answer is no. 21st Mortgage stopped accepting credit card payments, so you can’t use a card directly through their system.

Your only options are a linked bank account, whether through the online portal, phone, or autodraft. Some third-party bill pay services claim to accept cards for a fee, but that’s not the same as paying 21st Mortgage directly. It’s usually safer and cheaper to stick with your own bank account.

If you were hoping to earn credit card rewards on your mortgage, that’s not possible with this lender right now.

If you manage more than one loan, it’s worth seeing how CMG Mortgage payment and Flat Branch Mortgage payment options compare, since not every servicer handles cards the same way.

Setting Up Autodraft for Automatic Monthly Payments

Autodraft takes the guesswork out of paying on time. Once it’s set up, money gets pulled automatically every month or every two weeks. No more remembering due dates or worrying about late fees. If you just want to pay bill amounts fast without extra steps each month, this is the simplest long-term fix.

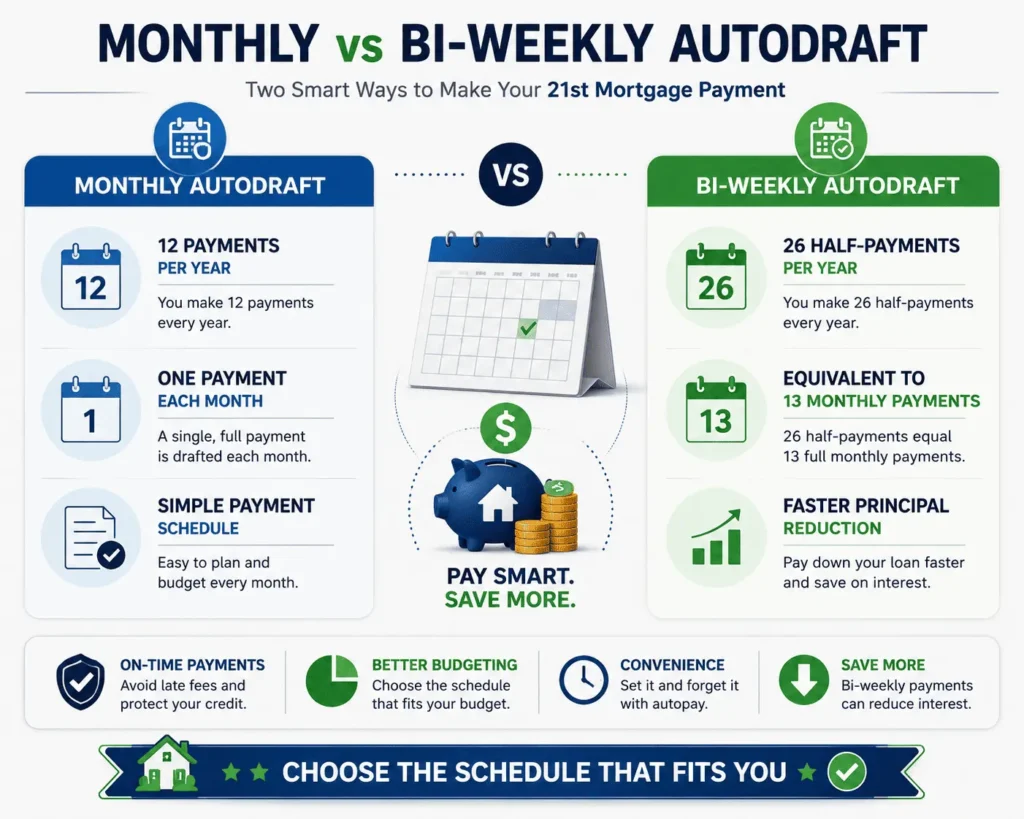

Monthly vs Bi-Weekly Autodraft — Which Is Better?

You get two choices with autodraft: monthly or bi-weekly. Monthly means one withdrawal each month, matching your regular due date. Bi-weekly means smaller payments taken out every two weeks instead.

Bi-weekly can actually save you money over time. Since there are 52 weeks in a year, you end up making the equivalent of 13 monthly payments instead of 12. That extra payment goes straight toward your principal, which can shorten your loan term.

Monthly autodraft is simpler if you get paid once or twice a month and want to match that schedule. Bi-weekly works better if you’re paid weekly or every other week and want to build equity faster.

There’s no wrong choice here. It really depends on your paycheck schedule and how aggressive you want to be about paying down the loan early.

For example, if your monthly payment is $600, bi-weekly autodraft pulls $300 every two weeks instead. Over a full year, that adds up to one extra full payment you probably wouldn’t have made otherwise. It’s a small change that can shave months, sometimes years, off a long-term loan.

What You’ll Need to Enroll in Autodraft

To sign up, fill out the Autodraft Payment Plan Authorization form. Here’s what to have ready:

- Your loan number

- A voided check or bank letter with your account details

- Your bank routing and account number

- Signed authorization from all borrowers on the loan

If the payment is coming from a savings account instead of checking, mark that on the form too. Once submitted, it usually takes one billing cycle to activate. Your payment amount may shift slightly over time if your taxes or insurance costs change, since those get folded into the draft.

Accessing Your 21st Mortgage Account Online

Your online account is where most of the payment action happens. It’s the fastest way to check your 21st mortgage payment history any time you want. It’s also where you’ll update contact info and track your loan balance over time.

Checking your mobile home online account takes less than five minutes once you’re set up. If you manage loans with more than one servicer, our guides on CMG Mortgage login, Flat Branch Mortgage login, and PHH Mortgage Center login cover similar steps for those companies.

Fixing Common Sign-In Errors

Login trouble usually comes down to a few simple issues. Here’s what to check first:

- Make sure your loan number matches exactly, including any leading zeros

- Double-check that Caps Lock isn’t on when typing your password

- Clear your browser cache if the page looks broken or won’t load

- Try a different browser if the portal keeps timing out

If you’ve forgotten your password, use the “Forgot Password” link on the login page. You’ll get a reset email within a few minutes for most accounts.

Still stuck? Call the general support line and a representative can verify your identity and help you back in. This usually takes less than ten minutes over the phone.

Understanding Fees, Grace Periods & Missed Payments

Nobody wants extra charges added to their loan. Knowing the rules ahead of time helps you avoid them completely.

21st Mortgage’s Late Fee Structure by State

Late fees on manufactured home loans vary depending on where you live. Most states use a percentage of your payment, while a few have flat fees instead.

| State or Fee Type | Fee Structure |

|---|---|

| Most states | Late fee set by loan agreement, typically 4-5% of payment |

| New York | Lesser of 2% or contract amount |

| AL, IA, MN, MO, OH, NJ, WA, WV, WY | No subordination fee applies |

| NSF (bounced payment) fee | Lesser of $20 or contract amount in most states |

Your exact fee schedule is listed in your original loan documents. If you’re not sure what applies to you, your monthly statement usually spells it out too.

Consequences of a Missed or Late Payment

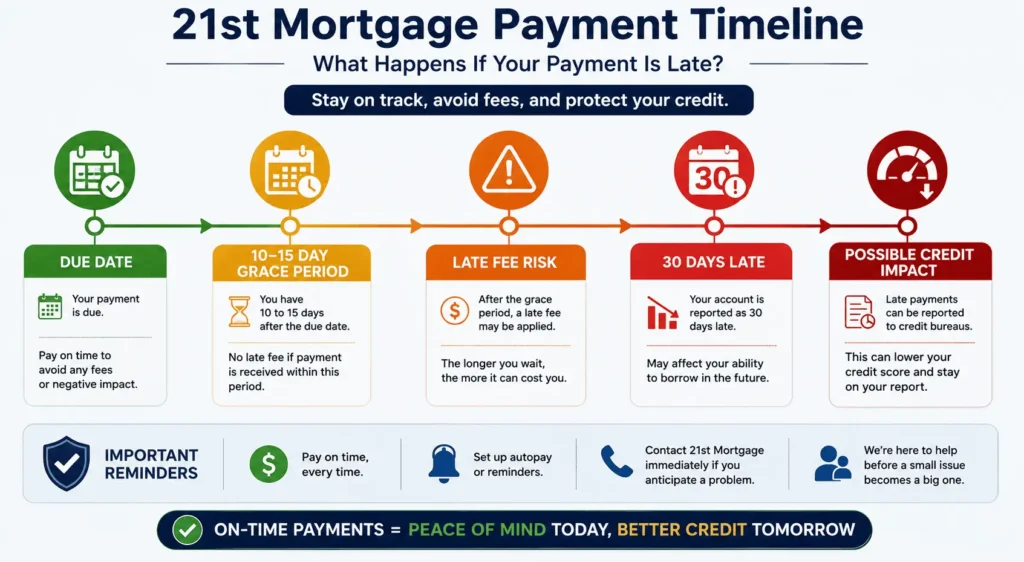

Most loans have a grace period of about 10 to 15 days after your due date. Paying within that window usually means no late fee at all.

Miss the grace period, and a late fee gets added to your balance. Missing several payments in a row can add real cost to your 21st mortgage payment and eventually put your home at risk of default. 21st Mortgage typically reports late payments to credit bureaus after 30 days past due.

The earlier you reach out about a payment problem, the more options you’ll have. Waiting until you’re several months behind makes things much harder to fix. If you know a payment is going to be late, call before the due date instead of after.

How to Pay Off Your 21st Mortgage Loan Early

Some borrowers want to close out their loan completely, whether that’s from selling the home or just paying it down faster. Your final 21st mortgage payment works differently than a regular monthly one, so it helps to know the steps ahead of time.

Requesting an Official Payoff Quote

You can’t just send extra money and guess the amount. Call the payoff department at 1-800-955-0021 extension 2900 and ask for a payoff quote.

This quote includes your remaining balance plus any interest that adds up daily until your target payoff date. It’s only good for a set number of days, so time your payment to match the quote. Payoff hours run Monday through Friday, 8 a.m. to 8 p.m. Eastern time.

Submitting Your Final Payoff Payment

Payoff funds usually need to go out as a cashier’s check, not a personal check. Mail it to 21st Mortgage Payment Processing, PO Box 477, Knoxville, TN 37901, ATTN: Payoff Dept.

You can also send it to the street address at 620 Market Street, Knoxville, TN 37902, same department. Once received, it takes a few business days to process and close the account. Ask for written confirmation once your loan shows as paid in full, just for your own records.

The Role of Escrow in Your Monthly Payment

Escrow is the part of your bill that covers property taxes and homeowner’s insurance. Instead of paying those in one huge chunk once a year, the cost gets split up and added to your monthly total.

21st Mortgage requires an escrow account on most loans. Every month, a portion of your 21st mortgage payment goes into this account. When your tax bill or insurance premium comes due, the company pays it directly from that pool of money.

This is why your payment can change even if your interest rate stays the same. If local property taxes go up, or your insurance premium increases, your escrow portion adjusts to match. The company reviews this once a year and sends a notice if your payment is changing.

It might feel frustrating when your bill goes up without warning, but it’s usually just an escrow adjustment. You can request an escrow analysis at any time if something looks off. This keeps you from getting a massive tax bill out of nowhere later.

Say your property taxes jump by $600 for the year. Spread across twelve months, that’s only an extra $50 added to your payment, instead of one painful lump sum in December. Most borrowers find this easier to plan around once they understand why it happens.

Struggling to Pay? Assistance Options Explained

Life happens, and sometimes a payment gets hard to make. If you can’t cover your 21st mortgage payment this month, the worst thing you can do is stay silent.

Call the borrower services line as soon as you know there’s a problem. 21st Mortgage has worked with borrowers on repayment plans, temporary payment reductions, and loan modifications depending on the situation. If you’re a servicemember, extra protections are available under federal law, and the company has a dedicated line for that.

Being upfront about job loss, medical bills, or a temporary income drop gives them something to work with. They’d rather set up a plan than start foreclosure, since that costs everyone more in the long run.

Document everything you send them, and always get agreements in writing. Verbal promises over the phone are easy to forget or misplace later. If you want a second set of eyes on your hardship paperwork before you send it, our editorial team can point you toward general resources — reach out anytime at james@allthings-mortgage.com.

21st Mortgage Contact Numbers for Every Situation

Different departments handle different problems. Calling the right number the first time saves you a lot of hold music.

General Loan & Payment Support

- Main customer service: 1-800-955-0021

- Automated phone payments: 1-866-380-0373

- Payoff department: 1-800-955-0021 ext. 2900

- Hours: Monday-Friday, 8 a.m.-8 p.m. Eastern (payment arrangement lines run until 9 p.m.)

These lines cover most everyday questions, from checking a balance to arranging a payment plan. If you’re calling about something specific, mention it right away so you get transferred to the right person faster. For other servicers, we’ve also broken down CMG Mortgage’s phone number and Flat Branch Mortgage’s phone number if you’re managing more than one loan.

Support for Military Servicemembers

Active-duty servicemembers and veterans have extra protections under the Servicemembers Civil Relief Act. 21st Mortgage has a specific team trained to handle these cases, including interest rate caps and foreclosure protections during active duty.

If this applies to you, mention your service status right when you call. You may need to provide deployment orders or other documentation to activate these protections. It’s worth doing even if you’re not currently struggling, just to have it on file.

Questions about anything covered here? You can also reach our team directly at james@allthings-mortgage.com.

Conclusion

Handling a 21st mortgage payment doesn’t have to feel confusing once you know your options. You can pay online, by phone, by mail, or set up autodraft so it happens automatically every month. We also covered fees, escrow, payoff steps, and who to call when something feels off. With this guide, you now have everything you need to manage your loan with real confidence.

Frequently Asked Questions

Can I pay my 21st Mortgage bill through doxo or other apps?

Yes, third-party bill pay services like doxo let you pay 21st Mortgage bills, but they may charge a fee unless you use a linked bank account. Paying directly through the company’s own portal or phone system is usually free and faster.

Is 21st Mortgage owned by Berkshire Hathaway?

Yes, 21st Mortgage Corporation is a subsidiary of Berkshire Hathaway. This ownership gives the company strong financial stability, which is part of why it remains one of the largest manufactured home lenders in the country today.

How can I view my payment history?

Log into the Account Access portal on 21stmortgage.com using your loan number and password. Your full payment history, including dates and amounts, is listed under your account dashboard, usually in the statements section.

What is 21st Mortgage’s NMLS number?

21st Mortgage Corporation’s NMLS number is 2280. You can verify this directly on the NMLS Consumer Access website, which confirms the company is licensed to originate manufactured home loans nationwide.

Why did my payment amount change?

Your payment likely changed because of an escrow adjustment. When property taxes or insurance premiums go up, the company recalculates your monthly amount to cover the new cost, usually sending a notice beforehand.