Choosing the Right Home Loan With Flat Branch Mortgage

Buying a home can feel overwhelming. Many people struggle with choosing the right lender and understanding costs. If you have ever wondered which mortgage fits your needs, you are not alone. This guide will explain how flat branch mortgage works and why it might be a solution for you.

You will learn about loan options, eligibility, fees, and the customer experience. Clear guidance helps borrowers avoid mistakes and surprises. By the end, you will understand if this lender is right for your home purchase. The goal is to simplify the process and make decision-making easier.

What Is Flat Branch Mortgage?

Flat Branch Mortgage is a lender that focuses on helping borrowers with a clear and guided approach. They combine personal support with online tools to make the process easier. Borrowers can discuss their needs directly with loan officers. This ensures a smoother experience compared to fully digital lenders.

Overview of the Lender

This lender offers multiple mortgage programs for a variety of buyers. Their focus is on clarity, support, and flexibility. Applications are reviewed carefully to match the borrower with the right loan. Many people choose them because of their hands-on approach.

Types of Borrowers It Serves

Flat Branch Mortgage works with first-time buyers, veterans, and borrowers seeking low down payment options. They also support USDA and FHA programs for specialized needs. Borrowers get guidance at every step, reducing confusion. The lender is suitable for anyone who wants clear support throughout the process.

Who Should Consider Flat Branch Mortgage?

Not all lenders fit every borrower’s situation. Flat Branch Mortgage works best for those who want guidance, clarity, and a variety of loan options. Knowing who benefits most can help you make the right choice.

Best for First-Time Homebuyers

First-time buyers often have questions about down payments and rates. Flat Branch Mortgage provides clear explanations to reduce stress. They help buyers plan finances before committing. This support makes the process more approachable.

Best for VA and USDA Borrowers

Veterans and rural homebuyers can benefit from specialized programs. VA loans often require no down payment, while USDA loans support rural home purchases. The lender guides borrowers through eligibility and documentation. These programs make homeownership more affordable for qualified applicants.

When Another Lender May Be a Better Choice

Some borrowers may prefer fully automated online lenders. Others may need large or specialty loans not widely available here. Comparing multiple lenders is always wise. Flat Branch Mortgage is ideal for borrowers who value guidance and personal support.

Mortgage Products Available Through Flat Branch Mortgage

Choosing the right loan type can affect your budget and eligibility. Flat Branch Mortgage offers multiple programs to fit different borrower needs. Understanding each option helps make an informed decision. Clear guidance ensures borrowers choose the best fit for their situation.

Conventional Loans

Conventional loans are standard financing options with flexible terms. Borrowers with stable income and credit often prefer them. These loans can be used for a variety of property types. Many people choose them for their competitive rates and predictability.

Benefits include:

- Flexible repayment terms

- Fixed or adjustable interest options

- Suitable for primary and secondary residences

FHA Loans

FHA loans help borrowers with lower credit scores or smaller savings. These programs are popular with first-time buyers. They require less upfront investment while offering reliable financing. Guidance from loan officers ensures borrowers meet all requirements.

Key points:

- Lower credit score flexibility

- Reduced down payment requirements

- Easier access for new buyers

VA Loans

VA loans support eligible military personnel and veterans. These programs often require no down payment. Borrowers can benefit from reduced fees and competitive rates. Flat Branch Mortgage helps with paperwork and eligibility verification.

Advantages:

- No large upfront payment

- Lower overall fees

- Support for veterans and active service members

USDA Loans

USDA loans target rural homebuyers and approved areas. They usually come with no down payment. Borrowers get affordable monthly payments and easier access. Guidance from the lender ensures smooth eligibility checks.

Highlights:

- No down payment required

- Rural property focus

- Lower monthly costs for qualified buyers

Low Down Payment Programs

Saving for a large down payment can delay homeownership. These programs allow smaller upfront investments. Flat Branch Mortgage helps first-time buyers take advantage of these options. It makes homeownership accessible sooner.

Advantages include:

- Reduced upfront cash

- Faster path to ownership

- Support for first-time and moderate-income buyers

Specialty Mortgage Solutions

Some borrowers need unique or specialized loan programs. Flat Branch Mortgage offers options for self-employed buyers or unusual properties. These programs ensure more people can qualify. Exploring all options helps borrowers find the best fit.

Examples:

- Self-employed financing

- Non-standard property loans

- Community-focused programs

Key Things to Know Before Applying

Preparation improves chances of approval and a smooth process. Flat Branch Mortgage expects borrowers to understand key requirements. Knowing these factors ahead helps prevent delays. Simple planning can save time and stress.

Minimum Credit Score Requirements

Credit score affects eligibility and interest rates. Stronger scores may access better programs and lower rates. Reviewing credit before applying is essential. Borrowers should correct errors and manage debt where possible.

Down Payment Expectations

Different loans have different upfront requirements. Some programs need more savings, others allow minimal down payment. Understanding this helps set a realistic budget. Planning early prevents surprises at closing.

Factors affecting down payment:

| Factor | Impact |

|---|---|

| Loan type | Conventional vs FHA vs VA |

| Credit score | Better scores can reduce required cash |

| Property value | Higher cost may increase down payment |

| Program selection | Each program sets its own rules |

Available States and Service Areas

Flat Branch Mortgage operates only in licensed states. Availability may vary by loan type and location. Checking eligibility before applying avoids wasted time. Lender websites and officers provide accurate state coverage info.

Required Documentation

Applications require proof of income, tax records, and identification. Preparing documents in advance speeds up processing. Organized paperwork reduces delays and follow-ups. The lender may request additional items based on the program.

Flat Branch Mortgage Rates, Fees, and Closing Costs

Borrowers need to understand full borrowing costs before committing. Interest, fees, and closing expenses add to the total loan cost. Flat Branch Mortgage provides clear guidance on these items. Transparent information helps plan finances accurately.

Mortgage Interest Rates

Rates determine monthly payments and total cost over time. Even small differences can impact long-term expenses. Borrowers should compare scenarios before committing. Loan officers help explain the influence of credit and program choice.

Closing Costs

Closing costs include administrative, appraisal, and legal fees. These vary depending on loan and property type. Knowing estimated amounts helps prevent last-minute surprises. Preparation improves financial planning.

Typical closing expenses:

- Appraisal fees

- Title and recording charges

- Processing costs

- Escrow fees

Lender Fees

Lender charges cover application, underwriting, and administration. These fees are standard across many lenders but may vary slightly. Understanding them upfront helps borrowers budget accurately. Transparency ensures no hidden surprises.

Factors That Affect Mortgage Pricing

Pricing depends on credit history, debt-to-income ratio, and loan type. Property location and occupancy status also matter. Better preparation can improve rates and reduce costs. Reviewing all factors helps make an informed decision.

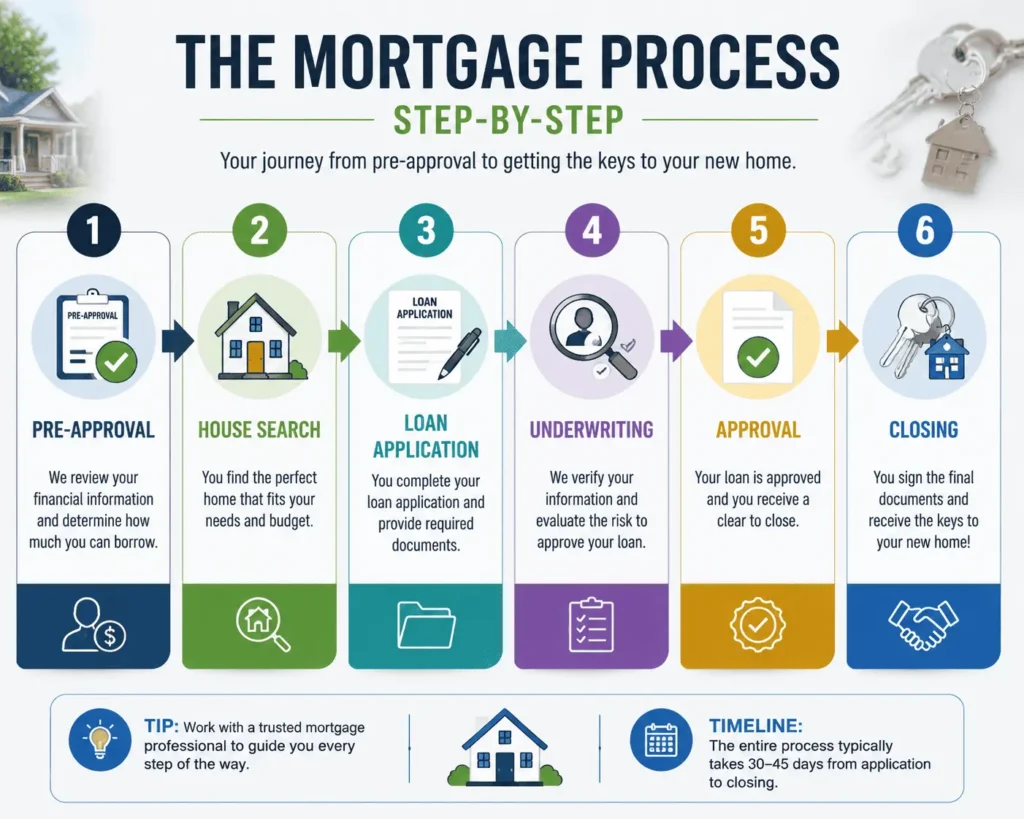

From Pre-Approval to Closing

Getting a mortgage is a step-by-step process. Understanding each stage helps reduce stress and avoid mistakes. Flat Branch Mortgage provides guidance throughout the journey. Knowing what comes next ensures a smoother experience.

Getting Pre-Approved

Pre-approval estimates how much you can borrow. Financial information, credit, and income are reviewed. This helps buyers understand their budget before house hunting. Pre-approved buyers are often stronger in negotiations.

Underwriting Process

Underwriting verifies all financial and property information. The lender ensures you meet program requirements. Additional documents may be requested during this stage. Responding quickly keeps the process on track.

Loan Approval and Closing

Once approved, the loan moves to closing. Borrowers review documents, sign papers, and complete payments. Ownership is officially transferred at closing. Guidance from Flat Branch Mortgage ensures this final step is smooth.

Pros and Cons of Flat Branch Mortgage

Understanding strengths and limitations helps make an informed choice. No lender is perfect for everyone. Knowing both sides prevents surprises. Flat Branch Mortgage provides a mix of programs and support.

Advantages

Many borrowers appreciate personal support and clear guidance. Multiple loan programs allow flexibility. First-time buyers and veterans often find this approach helpful. Personalized assistance improves confidence in decision-making.

Key benefits:

- Hands-on support

- Variety of financing options

- Guidance at every step

- Programs for different borrower types

Potential Drawbacks

Some borrowers prefer fully automated online services. Availability may differ by state or program. Specialty loans may not always be offered. Comparing lenders is still a wise strategy.

Common drawbacks:

- Limited availability in some areas

- Fewer fully digital tools

- Certain programs may not be offered

Flat Branch Mortgage Customer Reviews and Reputation

Customer feedback provides insights into experience quality. Reviews highlight strengths and areas for improvement. Trends across multiple reviews give a balanced picture. This helps borrowers set realistic expectations.

What Borrowers Like Most

Positive reviews mention helpful communication and guidance. Loan officers explain steps clearly. The process feels smoother when borrowers receive personal attention. Support at key milestones is often praised.

Highlights:

- Clear guidance

- Responsive communication

- Smooth application process

Common Complaints and Concerns

Some complaints involve documentation requests or processing timelines. Delays can occur if documents are missing or unclear. Understanding typical challenges prepares borrowers. Most issues are manageable with prompt response.

Common issues:

- Extra document requests

- Timeline adjustments

- Processing delays

Overall Satisfaction Trends

Borrowers with organized documents report smoother experiences. Communication quality influences satisfaction. Long-term trends suggest most customers are satisfied. Reviewing multiple sources provides confidence.

Flat Branch Mortgage vs Other Mortgage Lenders

Comparing lenders ensures you choose the best fit. Loan options, costs, and service differ across providers. Looking at several factors is better than choosing by a single feature. Flat Branch Mortgage often stands out for personal support and guidance.

Loan Options Comparison

Different lenders have varying program availability. Some focus on conventional loans; others emphasize government-backed programs. Comparing helps identify the best fit. Flat Branch Mortgage provides a balanced mix of options.

Cost and Fee Comparison

Costs vary depending on loan type and property. Reviewing interest, closing, and lender fees helps plan finances. Transparency is essential. Comparing costs ensures better decision-making.

Customer Experience Comparison

Service quality differs among lenders. Some focus on automation, others on personal guidance. Flat Branch Mortgage leans toward hands-on support. Evaluating experience helps match borrower preferences.

Conclusion

Choosing a mortgage is a major financial decision. As promised earlier, this guide explained flat branch mortgage, programs, costs, and borrower experience. The information here helps you decide with confidence. With preparation and guidance, applying for a mortgage can be smooth and predictable.

Frequently Asked Questions

Q1 What credit score is typically needed to qualify for a mortgage?

Credit score requirements depend on the loan program. Conventional loans often require stronger credit, while government-backed options may offer more flexibility. A higher score can also improve approval chances and borrowing terms.

Q2 Can I get pre-approved before finding a property?

Yes, pre-approval usually comes before house hunting. It helps determine your budget and shows sellers that you are a serious buyer. This step can also make the purchasing process more efficient.

Q3 How much down payment should I expect?

The required down payment varies by loan type and borrower profile. Some programs allow lower upfront costs, while others may require a larger contribution. Reviewing available options helps determine the best fit.

Q4 What documents are commonly required during the application process?

Most lenders request proof of income, tax records, bank statements, employment details, and identification. Having these documents ready can help avoid delays and make the review process smoother.

Q5 How long does it usually take to close a mortgage loan?

Closing timelines vary based on the loan type, documentation, and property details. Many transactions are completed within a few weeks, though some may take longer if additional verification is required.

Q6 Are interest rates the only cost to consider when comparing mortgages?

No. Borrowers should also review closing costs, lender fees, and other related expenses. Looking at the total cost of borrowing provides a more accurate comparison than focusing only on the interest rate.

![PHH Mortgage Services: Complete Guide [2026]](https://indianamortgagerate.com/wp-content/uploads/2026/05/phh-mortgage-services-loan-transfer-768x512.webp)