CMG Mortgage Rates Explained: Smart Ways to Secure the Best

You searched CMG mortgage rates late at night, hoping for one clear number, and got vague pages instead. That happened to me too the first time I researched a lender for a client who wanted a straight answer, not a sales pitch. Every page seemed to talk around the topic instead of through it, and the silence on real numbers only added to the stress.

This guide breaks down the pricing in plain terms, section by section, so you are not left guessing. You will learn how CMG’s numbers compare to the market, why the lender keeps them private, and what actually moves your quote up or down. You will also see where real savings hide inside CMG’s own programs. By the end, you will know exactly what to ask before you lock anything in.

CMG Mortgage Rates vs. the National Average

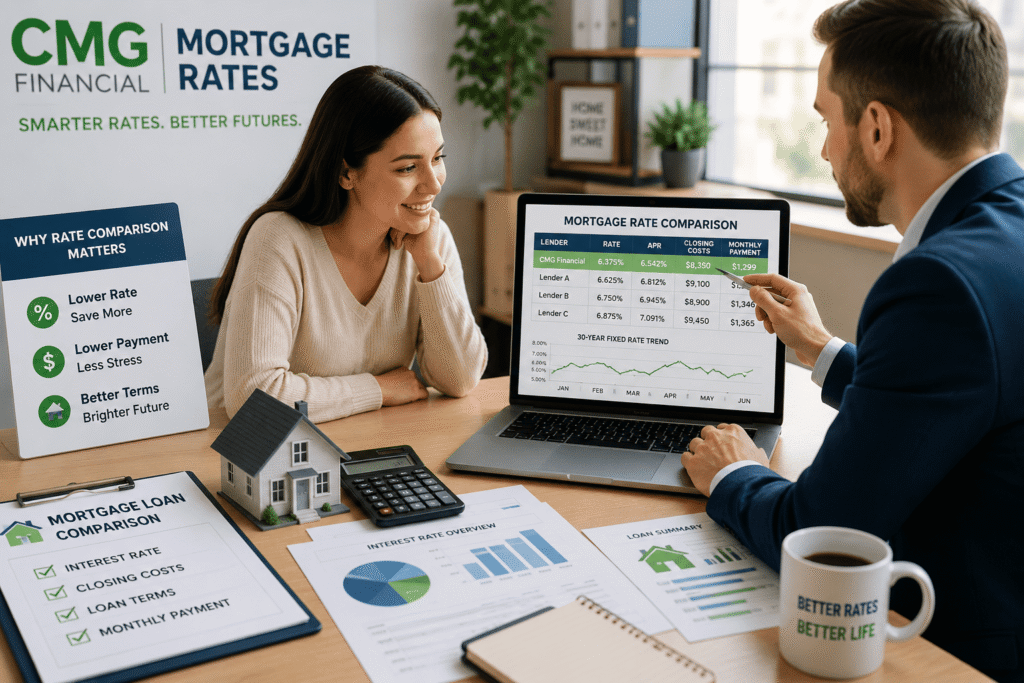

CMG Financial priced loans close to the market average last year. Its typical rate landed around 6.8 percent, while the broader market average sat closer to 6.55 percent. That gap is small on paper, but it can still add up over the life of a large loan balance.

Most CMG borrowers land in the 6 to 7 percent bucket, which lines up with where most lenders sit right now. Closing costs tend to run a bit higher than average too, often near $9,600 on a standard 30 year loan compared to roughly $8,350 industry wide. This pattern shows up consistently across recent federal loan disclosure data, which tracks originations from thousands of lenders each year. None of this makes CMG a bad choice on its own.

It simply means shopping around still pays off, even when you are working with a well known, established lender. A quarter point difference in your interest cost sounds small on a rate sheet, but it adds up to real money over a 30 year term. Two lenders can quote you nearly the same headline number and still land on very different total costs once fees are factored in. If you want the full picture beyond just pricing, our CMG mortgage review covers what first time and repeat buyers can expect from the process overall.

Why CMG Doesn’t Publish Advertised Rates

Here is something most reviews skip over completely. CMG does not list sample rates on its website the way some competitors do. You have to start an application or speak with a loan officer directly to see real numbers tied to your file. If you want to skip the hold music, our CMG mortgage phone number guide lists verified contact paths for reaching a loan officer fast.

This practice is common among mortgage banks that price loans individually based on credit, income, and property details rather than a flat published sheet. It is not automatically a red flag. It does mean you should never assume a rate you saw somewhere else, even on a comparison site, will apply exactly to your own situation.

The smarter move is to request a written quote early in the process. Ask your loan officer for the rate, the discount points, and the closing fees together in one document, not as separate pieces. That way you are comparing full offers side by side instead of guessing based on a headline number.

How Often CMG Mortgage Rates Change

Mortgage pricing moves daily, and sometimes it shifts twice within the same day. CMG adjusts its rate sheets based on bond market activity, Federal Reserve signals, and overall investor demand for mortgage backed securities. A number you see this morning can look noticeably different by the middle of the week.

This is exactly why CMG mortgage rates are never truly fixed until you formally lock them in. Locking protects your quoted number for a set window, usually somewhere between 30 and 60 days depending on the loan program. Once a rate is locked, you can track its status anytime through your account, and our CMG mortgage login walkthrough shows exactly where to look. If you are still comparing lenders, ask directly how long a quoted price stays valid before it needs to be refreshed.

Keep in mind that a rate lock is not free protection forever. Some lenders charge a small fee to extend a lock if your closing date slips. Understanding this upfront helps you plan your timeline instead of getting surprised later.

Factors That Affect Your CMG Mortgage Rate

Your personal loan file shapes the exact number CMG offers you, far more than any published average ever will. Two neighbors buying similar homes can walk away with different pricing simply because their profiles are not identical. A handful of factors carry far more weight than the rest, and understanding them puts you in a stronger negotiating position.

Credit Score

Your credit score is one of the biggest levers in the entire pricing formula. Borrowers with scores above 740 usually see CMG’s best available pricing tier. Scores in the 620 to 680 range can still qualify for many programs, but the rate typically runs higher to offset added lender risk. Paying down credit card balances a few months before applying, even partially, can nudge your score into a better tier without any drastic changes to your budget.

Down Payment and Loan-to-Value

A bigger down payment lowers your loan-to-value ratio, and lenders consistently reward that with better pricing. Putting down 20 percent also skips private mortgage insurance entirely on conventional loans. Even a modest 5 to 10 percent down payment can beat the minimum down payment options when it comes to pricing. Sellers offering credits, gift funds from family, and down payment assistance programs can all help you reach a stronger tier without draining your savings account.

Debt-to-Income Ratio

Lenders compare your total monthly debt against your gross monthly income before setting a final number. CMG generally wants this ratio under 45 percent for most conventional loan approvals. A lower ratio signals less risk to the lender, and that often translates into friendlier pricing on your rate.

Loan Type and Term

A 15 year loan usually prices lower than a 30 year loan because the lender takes on less long term risk over a shorter payoff window. Government backed loans like FHA or VA can also price differently than conventional loans depending on current market conditions. The right term for you really depends on your monthly budget and how long you plan to stay in the home. Someone planning to sell within five years might lean toward an adjustable option, while a buyer settling in long term usually prefers the stability of a fixed term.

CMG Mortgage Rates by Loan Type

CMG offers several distinct loan programs, and pricing shifts depending on which one actually fits your borrower profile. Here is a quick side by side view to help you compare options before you talk to a loan officer.

| Loan Type | Typical Rate Positioning | Best For |

|---|---|---|

| Conventional | Market average pricing | Buyers with strong credit and steady income |

| FHA | Slightly below conventional in some cases | First time buyers with lower credit scores |

| VA | Often competitive, no down payment needed | Eligible veterans and active service members |

| USDA | Low rates in eligible rural areas | Buyers in qualifying rural zip codes |

| Jumbo | Can run higher due to loan size | Buyers financing above conforming limits |

| ARM | Lower start rate, adjusts later | Buyers planning to move or refinance early |

CMG also offers a 1 percent down payment option, plus specialty products built for medical professionals and self employed borrowers with non traditional income. Each program carries its own pricing structure and eligibility rules. Ask your loan officer for a full side by side comparison before you settle on one path. Bringing a printed copy of this table to your first conversation can help keep the discussion focused and save you a follow up call.

CMG’s List and Lock Rate Lock Program

CMG runs a unique feature called List and Lock that most competitor reviews never mention. It lets a seller offer buyers a below market rate on a specific listed home, funded through a seller paid credit at closing. Buyers still get several loan options under this program, including conventional, FHA, VA, and select adjustable rate mortgages.

The lock typically holds for 60 days starting from the listing date. If a buyer closes within that window, they receive the advertised rate instead of qualifying at the day’s standard market pricing. This stands out as one of the few real rate incentives tied directly to a specific property rather than a generic site wide promotion.

If you come across a home listed with this program, ask your real estate agent for the exact rate sheet attached to that property. It can translate into real monthly savings compared to standard market pricing on a similar home nearby.

Sellers like this tool because it widens their buyer pool without cutting the listing price. Buyers benefit because the lock happens before they even submit an offer, which removes some guesswork from budgeting. It will not appear on every listing, so it pays to ask early rather than assume it applies.

How to Get the Lowest CMG Mortgage Rate

A handful of simple habits genuinely move the needle when you are chasing a lower quote from CMG. Try each of these before you commit to any single offer.

- Check your credit report for errors and dispute them before you formally apply.

- Save toward a larger down payment if your closing timeline realistically allows it.

- Ask about discount points and run the break even math on your own.

- Compare a full loan estimate document, not just a single quoted number.

- Get written quotes from at least two other lenders on the same day for a fair comparison.

Feel free to email james@allthings-mortgage.com if you want a second set of eyes on a loan estimate before you sign anything binding. A short outside review can catch hidden fees that quietly inflate your real cost.

CMG Mortgage Rate Pros and Cons

CMG brings real strengths to the table that go beyond just a number on a page. The lender offers a wide range of home loans, including USDA options and a crowdfunding tool that helps with down payments. Service quality also scores above the industry average in recent national satisfaction studies.

The tradeoffs are worth knowing too before you commit. CMG does not publish rates upfront, so shopping around takes one extra step compared to lenders with public rate sheets. Total loan costs have also run higher than the industry median in past reported data, which makes comparing complete offers even more important than usual. First time buyers in particular should budget extra time for this step, since a rushed comparison often means missing a cheaper option elsewhere.

None of these tradeoffs are dealbreakers on their own. They simply mean you should treat CMG the same way you would treat any lender, with a full side by side comparison rather than a quick glance at one number. The strongest borrowers are the ones who ask for everything in writing before they commit.

Once your loan closes, staying on top of your monthly bill matters just as much as the rate you locked. Our guide to CMG mortgage payment options walks through the easiest ways to pay each month without missing a due date.

Conclusion

Shopping for CMG mortgage rates does not have to feel like guesswork anymore once you know where to look. You now understand why CMG keeps its numbers private, what actually shapes your personal rate, and where real savings hide inside programs like List and Lock. Use the comparison steps covered above before you sign anything, and always read your full loan estimate line by line. That is the promise this guide set out to keep from the very first paragraph.

CMG Mortgage Rates FAQs

What is CMG Financial’s current average mortgage rate?

CMG’s average rate has tracked close to the national market average recently, often within a quarter point either way. Your exact number depends heavily on credit score, down payment, and loan type. Request a personalized quote today for the most accurate figure available. Rates shift daily based on broader market conditions.

Does CMG Financial publish rates online?

No, CMG does not list sample rates publicly on its main website like some competitors do. You need to start an application or speak with a loan officer to see real numbers tied to your file. This is standard practice among many mortgage banks nationwide. A written quote gives you the clearest possible picture.

How do I lock in a CMG mortgage rate?

You lock a rate after receiving a formal quote, usually once you are officially under contract on a home. Locks typically hold for 30 to 60 days depending on the loan program you choose. Ask your loan officer about extension options if your closing date shifts unexpectedly. Locking protects you from sudden daily market swings.

What credit score do I need for the best CMG rate?

A score above 740 typically unlocks CMG’s best available pricing tier on most loan programs. Scores between 620 and 680 can still qualify for many options, just at a higher cost. Lower scores usually mean higher pricing to offset added lender risk. Improving your score before applying can meaningfully lower your rate.

How does CMG’s rate compare to other lenders?

CMG generally prices near the broader market average, based on recent origination data reviewed above. Some lenders undercut CMG slightly on rate, while others charge more in overall fees. Comparing full loan estimates side by side remains the only reliable way to know for certain. Email james@allthings-mortgage.com if you want help reading through a comparison.

![PHH Mortgage Services: Complete Guide [2026]](https://indianamortgagerate.com/wp-content/uploads/2026/05/phh-mortgage-services-loan-transfer-768x512.webp)