21st Mortgage Review: What Manufactured Home Buyers Need to Know

Buying a manufactured or mobile home comes with financing questions that regular mortgage guides never really answer. Maybe you searched for a lender who understands manufactured housing and landed on 21st Mortgage, only to find confusing rate ranges and unclear rules about credit scores. I ran into this same wall while helping a family member shop for a manufactured home loan last year, and the lack of straight answers was frustrating.

This guide clears up the confusion. You will learn how the loans work, what rates and fees to expect, who qualifies, and how the whole process runs from application to closing. By the end, you will know exactly whether this lender fits your situation.

What Is 21st Mortgage Corporation?

21st Mortgage is one of the largest lenders in the country that focuses only on manufactured and mobile homes. The company started in 1995 and is based in Knoxville, Tennessee. It has funded loans for more than 240,000 borrowers across the United States.

Unlike big banks, this lender does not offer regular home loans, FHA loans, or VA loans. It sticks to one lane: manufactured housing. That focus is why many buyers turn to 21st Mortgage when other lenders turn them away.

| Feature | Details |

|---|---|

| NMLS ID | 2280 |

| Headquarters | Knoxville, Tennessee |

| Loan Focus | Manufactured and mobile homes |

| States Served | 46 states (not AK, HI, MA, RI) |

| Interest Rate Range | About 7% to 14% |

| Minimum Credit Score | None required |

| Minimum Down Payment | 0% for well-qualified buyers |

Loan Types Offered by 21st Mortgage

This lender offers a few loan paths depending on what kind of home you are buying and where it will sit.

Chattel (Personal Property) Loans

A chattel loan treats your manufactured home like personal property instead of real estate. This is common when you own the home but not the land underneath it. Rates on chattel loans tend to run higher because the collateral is considered riskier.

Land-Home (Real Property) Loans

If you are buying the home and the land together, you may qualify for a land-home loan instead. These loans often come with slightly better terms and longer repayment periods. You can finance up to 30 years if the land and home are purchased as one package.

Refinance & Cash-Out Refinance

Current borrowers can refinance an existing loan or pull cash out of their home equity. The minimum loan amount for refinancing is $25,000, and you need at least a 5% down payment. Cash-out refinancing requires a credit score of 600 or higher and is not offered in Texas.

21st Mortgage Interest Rates and Fees

Rates from 21st Mortgage usually fall between 7% and 14%, depending on your credit profile and loan type. That range is higher than what you would see on a typical site-built home mortgage. Manufactured home loans carry more risk for lenders, so the higher rate reflects that.

Your exact rate depends on your credit score, down payment size, and whether the loan is chattel or land-home. Borrowers with strong credit and larger down payments usually land on the lower end of that range.

Closing Costs

Expect to pay fees for loan origination, credit checks, title work, and escrow services. Most of these costs can be rolled into your loan so you do not pay everything upfront. Just remember that rolling costs into the loan means paying interest on them over time. Appraisal and recording fees usually cannot be financed this way.

Eligibility Requirements

Qualifying for a loan through this lender works a bit differently than a conventional mortgage.

Credit Score Requirements

21st Mortgage does not set a strict minimum credit score for most loans. That said, your score still shapes your rate and down payment. Buyers with scores below 575 usually need a much larger down payment to get approved.

Down Payment Requirements

Well-qualified buyers with strong credit can sometimes get financing with no down payment at all. If your credit score sits below 575, expect a down payment of around 35%. This gap is one of the biggest factors buyers overlook when budgeting.

State Availability and Restrictions

This lender serves 46 states but skips Alaska, Hawaii, Massachusetts, and Rhode Island entirely. There are also extra restrictions in specific counties, including parts of Illinois. Some park model homes are excluded in states like Kentucky, Montana, and Vermont.

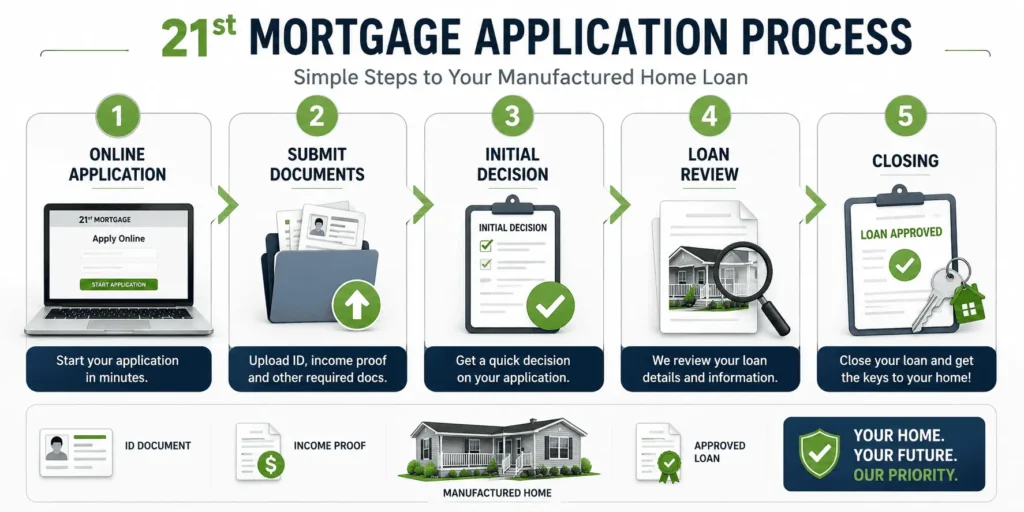

How to Apply for a 21st Mortgage Loan

The application process is fully digital, and there is no prequalification step. That means submitting a full credit application triggers a hard credit inquiry right away.

Documents You’ll Need

You will need to gather several pieces of information before applying.

- Full name, date of birth, and current address

- Social Security number or taxpayer ID

- Proof of income and employment

- Details about the home, including size and year built

- Information about the land or community where the home will sit

- Purchase price and planned down payment amount

Approval Timeline

Most borrowers hear back on an initial decision within 24 hours of applying. After that, you get about 60 days to submit full documentation. The entire process from application to closing usually takes four to eight weeks, based on how fast paperwork comes together.

Mobile Home Insurance Through 21st Mortgage

Many borrowers do not realize this lender also connects buyers with insurance for their manufactured home. This coverage is often required as part of your loan agreement. Reviews from real customers show mixed experiences here, especially around storm and wind damage claims.

Several borrowers reported slow claim payouts after tornado or wind damage to their homes. If insurance is bundled into your loan, it is worth comparing outside quotes before you commit. Shopping around for your own policy can sometimes get you better claim coverage at a similar price.

Managing Your Loan — Payments, Servicing & Customer Service

Once your loan closes, 21st Mortgage services the loan directly rather than selling it off. Payments can be made online, by phone, or by mail through their processing center. Customer service is available Monday through Friday, from 9 a.m. to 6 p.m. Eastern time.

If you are comparing how different servicers handle online payments, our CMG Mortgage Payment guide breaks down similar digital options across lenders. For borrowers who prefer speaking to someone directly, our CMG Mortgage Phone Number guide shows how to skip the automated menus and reach a real person faster. You can also see how login portals typically work in our PHH Mortgage Center Login walkthrough, since most servicers follow a similar setup.

If you have questions specific to your loan file, you can also reach out through email at james@allthings-mortgage.com for guidance.

Is 21st Mortgage Legit? BBB Rating and Customer Reviews

Yes, 21st Mortgage is a licensed and legitimate lender with an A+ rating from the Better Business Bureau. It has been in business for over 25 years and services billions of dollars in loans. That said, legitimate does not always mean flawless.

Customer reviews across platforms like ConsumerAffairs and WalletHub show a common pattern. Origination experiences tend to be smooth, with borrowers praising helpful loan officers. Servicing complaints are more frequent, especially around collection calls when payments run late. A few reviewers also flagged slow escrow refunds after paying off their loan early.

Pros and Cons of 21st Mortgage

Weighing the good and bad helps you decide if this lender matches your needs.

Pros:

- No minimum credit score requirement for most loans

- Up to 100% financing available for qualified buyers

- No private mortgage insurance required

- Fast initial approval decisions, often within 24 hours

Cons:

- Interest rates run higher than conventional mortgages

- No physical branch locations for in-person help

- Aggressive collection communication reported by some borrowers

- Not available in four states and select counties

21st Mortgage vs. Vanderbilt Mortgage

Buyers often confuse these two lenders because both focus on manufactured housing and share the same parent company, Clayton Homes. Vanderbilt Mortgage tends to work closely with Clayton-built homes sold through its own retail network. 21st Mortgage, on the other hand, finances homes from a wider range of retailers and private sellers.

Rate structures between the two are similar, but eligibility can differ based on which retailer sold the home. If you bought your home through a Clayton-affiliated dealer, Vanderbilt might offer smoother processing. For homes purchased elsewhere, 21st Mortgage usually has the broader reach.

21st Mortgage vs. Other Manufactured Home Lenders

Rocket Mortgage and Better both offer financing for manufactured homes, but only if the home sits on a permanent foundation. That rules out many chattel loan buyers who do not own the underlying land. This is where 21st Mortgage stands out, since it accepts homes without permanent foundations too.

If you are researching other servicers while comparing your options, our full CMG Mortgage review and Flat Branch Mortgage guide cover how traditional lenders structure their loans. For borrowers weighing rate differences across the market, our Flat Branch Mortgage Rates breakdown is a useful comparison point. You can also check our PHH Mortgage Services Complete Guide if your loan gets transferred to a different servicer down the road.

Is 21st Mortgage Right for You?

This lender makes the most sense for buyers purchasing a manufactured or mobile home who got turned down elsewhere. It also fits buyers with limited credit history, since there is no strict minimum score. If low rates matter more to you than approval flexibility, a conventional lender may serve you better.

Conclusion

Choosing a lender for a manufactured or mobile home does not have to feel confusing anymore. This guide walked through exactly how 21st Mortgage works, from loan types and rates to eligibility and the full application process. You now have the details needed to compare this lender against other options with confidence. Whether you move forward with them or not, you are making that decision with clear information instead of guesswork.

Frequently Asked Questions

Does 21st Mortgage require a down payment?

Not always. Well-qualified buyers with strong credit can sometimes finance 100% of the purchase price. Buyers with credit scores below 575 typically need a down payment of around 35%. Your exact requirement depends on your credit profile and loan type.

Can I refinance my loan with 21st Mortgage?

Yes, refinancing is available with a minimum loan amount of $25,000. You will need at least a 5% down payment to qualify. Cash-out refinancing requires a credit score of 600 or higher and is unavailable in Texas.

Does 21st Mortgage finance homes without land?

Yes, chattel loans let you finance the home only, without owning the land beneath it. This option works well for homes placed in manufactured home communities. Rates on chattel loans tend to be slightly higher than land-home loans.

How long does approval take?

Most applicants get an initial decision within 24 hours of applying. Full approval and closing usually take four to eight weeks total. Timelines can shift based on how quickly you submit required documents.

Is 21st Mortgage available in every state?

No, it serves 46 states but skips Alaska, Hawaii, Massachusetts, and Rhode Island. Some counties and loan types face extra restrictions too. Always confirm availability in your specific area before applying.