Mastering Your Flat Branch Mortgage Payment: Smart Ways to Save More and Pay Less

Every month, that mortgage bill shows up — and for a lot of Flat Branch borrowers, the first question is simple: am I paying this the right way? Maybe your payment changed this year and you are not sure why, or maybe you want to pay extra but do not know how to make it count. Maybe life got hard and you missed a due date and now you are wondering what happens next. These are real situations, and they happen to real homeowners all the time.

This guide on flat branch mortgage payment walks you through everything — from what is inside your monthly bill to how to pay it, when it is late, how to pay it off faster, and what to do when you need help. By the end, you will know exactly where to go, what to do, and how to keep your loan on track.

What Your Flat Branch Mortgage Payment Actually Covers

Most people think their mortgage payment is just the loan amount split into monthly chunks. It is actually more than that. Your payment covers four main things — and knowing each one helps you understand why the number looks the way it does.

Principal is the part that pays down your actual loan balance. Interest is what Flat Branch charges you for borrowing that money. Taxes and insurance are collected monthly and held in an escrow account until the bills come due. Together, these four parts are called PITI — Principal, Interest, Taxes, and Insurance.

Your escrow account is reviewed once a year by Flat Branch. If your property taxes or homeowners insurance went up, your monthly payment will go up too — even if your interest rate did not change. This is one of the most common reasons borrowers see their payment increase without warning.

Private mortgage insurance, or PMI, is added to your payment when your down payment was less than 20%. It protects the lender, not you. Once your loan balance drops to 80% of your home’s value, you can request PMI removal — it does not always drop off automatically, so you have to ask.

How Your Loan Type Affects Your Monthly Payment Amount

Not every Flat Branch borrower has the same type of loan, and that matters for your payment. A conventional loan, an FHA loan, a VA loan, and a USDA loan all have different rules, rates, and costs built in.

FHA loans carry a monthly mortgage insurance premium that stays for the life of the loan in most cases. VA loans have no PMI at all, which keeps payments lower for eligible veterans. USDA loans are zero-down but include a small annual fee rolled into the payment. Conventional loans offer the most flexibility once you build enough equity.

Your loan term makes a big difference too. A 15-year loan has higher monthly payments but you pay far less interest over time. A 30-year loan keeps payments lower each month but costs more in total interest. The right choice depends on your budget and your long-term goals.

How to Make Your Flat Branch Mortgage Payment

Flat Branch gives you several ways to pay. The method you choose can affect how fast your payment is processed and whether it arrives on time.The fastest and most reliable way to pay online is through the servicing center. If you need help accessing your account, resetting credentials, or signing in for the first time, check our Flat Branch Mortgage Login guide before making a payment.

Servicing Digital Online Portal

The fastest and most reliable way to pay online is through the Flat Branch servicing center at loansphereservicingdigital.bkiconnect.com/fbhl. You log in with your username and password, choose your payment amount, and submit. The portal is available 24 hours a day, seven days a week.

You can make a one-time payment or schedule a recurring payment from the same screen. If you ever have trouble logging in near your due date, call the servicing team right away rather than waiting. Portal outages are rare but they do happen, and waiting could push you past your grace period.

Flat Branch Servicing Mobile App

The Flat Branch Servicing app is available on both iOS and Android. You can use it to view your current balance, check payment history, download loan documents, and make payments directly from your phone.

One important thing to know — after a January 2024 update, the app removed the option to make a separate standalone principal-only payment. You can still adjust your regular monthly payment amount inside the app, but if you want to send an extra lump sum to principal only, you need to do that through the online portal instead.

Autopay Setup — Step by Step

Setting up autopay is the single smartest thing you can do to protect your credit score and avoid late fees. Log into the Servicing Digital portal, go to Account Details, and click Schedule Recurring Payments. You will need your bank routing number and account number to complete the setup.

Autopay pulls funds from your bank account on the date you choose each month. Once it is active, check the app after each payment to confirm it went through. Do not assume it processed — verify it, especially in the first month after setup.

Pay by Phone or Mail

If the portal is down and your due date is close, paying by phone is your best backup. Call Flat Branch servicing at 877-350-0350 and a team member can process your payment over the phone.

Mail payment is the slowest option and carries real risk near your due date. If you send a check, write your loan account number clearly on the memo line. Your home address alone is not enough for them to match it to your account. Allow at least five to seven business days for mail to arrive and be processed.

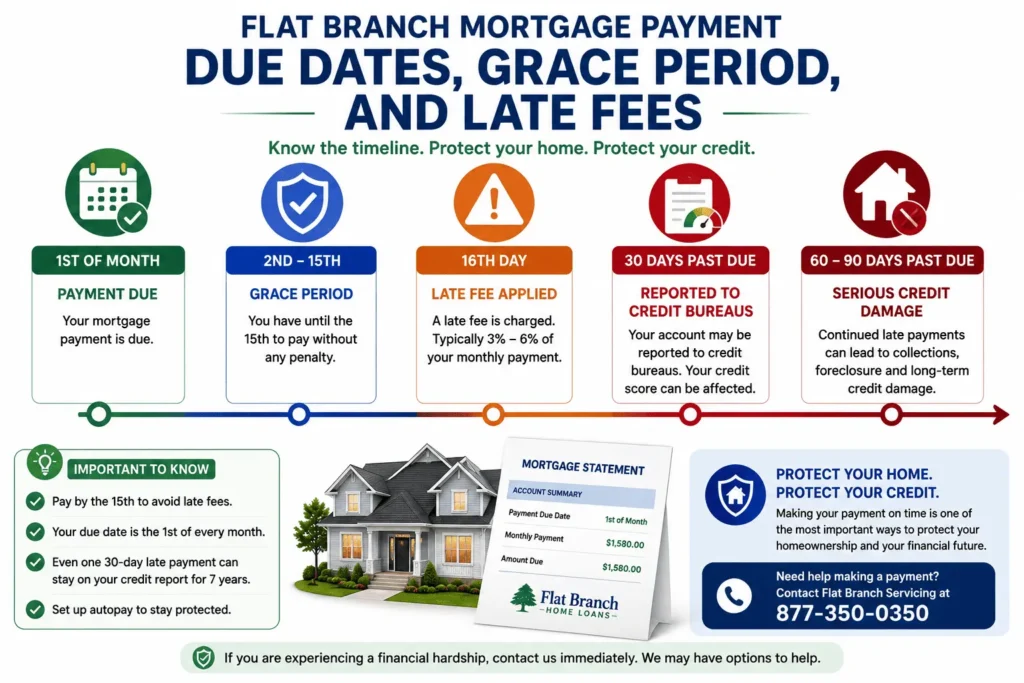

Flat Branch Mortgage Payment Due Dates, Grace Period, and Late Fees

Your payment is due on the first of every month. Most borrowers have until the 15th to pay without any penalty — that 15-day window is your grace period.

The day after the grace period ends, a late fee is applied. Based on standard mortgage terms, this is typically between 3% and 6% of your monthly payment amount. On a $1,500 payment, that could mean a $45 to $90 charge added immediately.

Here is the timeline that matters most for your credit:

| Day | What Happens |

|---|---|

| 1st | Payment due |

| 2nd–15th | Grace period — no penalty |

| 16th | Late fee applied |

| 30 days past due | Reported to credit bureaus |

| 60–90 days past due | Serious credit damage begins |

Your credit score is safe as long as you pay before the 30-day mark. One late fee hurts your wallet. A 30-day late mark hurts your credit for years.

If You Cannot Make Your Payment — Do This Immediately

The worst thing you can do is go quiet. Call Flat Branch servicing at 877-350-0350 the moment you know you cannot make your payment on time. They have options — but only if you reach out before the problem gets worse.

Forbearance lets you temporarily pause or reduce your payments during a financial hardship. It is not automatic — you have to request it and explain your situation. A repayment plan lets you catch up on missed payments gradually over time rather than all at once. Loan modification is a longer-term solution that can permanently change your rate or term if you qualify.

Acting before 30 days is everything. After 30 days, the late payment hits your credit report and the path back gets harder and more expensive.

How to Make Extra Principal Payments on Your Flat Branch Loan

Paying extra toward your principal is one of the most powerful moves a homeowner can make. Every extra dollar you send reduces your balance, which means less interest charged next month — and every month after that.

To apply an extra payment correctly, log into the Servicing Digital portal and specify that the extra amount should go to principal only. If you do not label it, the servicer may apply it as a regular payment for next month instead, which does not give you the same benefit.

Because of the January 2024 app update, principal-only payments cannot be made as a separate transaction inside the mobile app. Use the online portal or call the servicing team directly at 877-350-0350 to handle this.

A biweekly payment strategy works like this — instead of one full payment per month, you pay half your monthly amount every two weeks. That adds up to 26 half-payments per year, which equals 13 full payments instead of 12. That one extra payment per year adds up to years off your loan.

How Much Can Extra Payments Actually Save You?

The numbers on extra principal payments are hard to ignore. On a $250,000 loan at 6.5% interest over 30 years, your standard monthly payment is around $1,580.

Adding just $200 extra per month toward principal cuts approximately six years off your loan term and saves over $60,000 in total interest. That is real money staying in your pocket instead of going to the lender.

How to Reduce or Pay Off Your Flat Branch Mortgage

If your monthly payment feels too high, you have real options — and some of them do not require starting over from scratch.

PMI removal is the first place to look. Once your loan balance reaches 80% of your home’s appraised value, contact Flat Branch servicing and request PMI cancellation. This can save $100 to $200 or more per month depending on your loan size — without refinancing.

Is Refinancing Worth It Right Now?

Refinancing makes sense when the math works in your favor. Flat Branch has a Refinance Guarantee program — if you refinance before March 31, 2026 and rates drop again before September 30, 2027, you can refinance a second time at no extra cost. You need six consecutive on-time payments to qualify.

The break-even formula is simple. Divide your total closing costs by your monthly savings. If closing costs are $4,000 and you save $200 per month, you break even in 20 months. If you plan to stay in the home longer than that, refinancing makes financial sense.

How to Request a Flat Branch Mortgage Payoff Quote

When you are ready to pay off your loan — whether through a sale, a refinance, or your own savings — you need an official payoff request first. Call Flat Branch servicing at 877-350-0350 or submit the payoff request form through their website.

Request the quote no more than 48 hours before you plan to send the funds. Your balance changes daily because interest accrues every day, so an older quote will give you the wrong number. If you have autopay active, cancel it at least three business days before your payoff date to prevent an extra draft from going through.

Conclusion

Managing your flat branch mortgage payment does not have to feel like a guessing game. You now know exactly what is inside your bill, how to pay it the right way, what happens when life gets in the way, and how to cut years off your loan with smart extra payments. Every step in this guide was built to give you real answers — not general advice. Take one action today, whether that is setting up autopay, making an extra principal payment, or calling to ask about your options — your future self will thank you.

Frequently Asked Question

How can I make an online mortgage payment?

You can make an online mortgage payment through the servicing portal. After signing in, you can submit a one-time payment, schedule future payments, or enroll in automatic monthly payments directly from your bank account.

What happens if a mortgage payment is late?

Most mortgage loans include a grace period after the due date. Once that period ends, a late fee may be charged, and payments that become 30 days past due can be reported to credit bureaus, potentially affecting your credit score.

Can I make extra principal payments?

Yes, borrowers can make extra principal payments to reduce their loan balance faster. Doing so may lower total interest costs and help pay off the mortgage sooner than the original loan term.

Why did my Flat Branch mortgage payment increase?

A Flat Branch mortgage payment may increase because of higher property taxes, homeowners insurance premiums, escrow shortages, or mortgage insurance costs. These changes can affect the monthly amount even if the interest rate stays the same.

How do I request a Flat Branch mortgage payoff quote?

To obtain an official payoff statement, contact the servicing department or submit a request through the online portal. A payoff quote provides the exact amount needed to fully satisfy the loan, including any accrued interest.